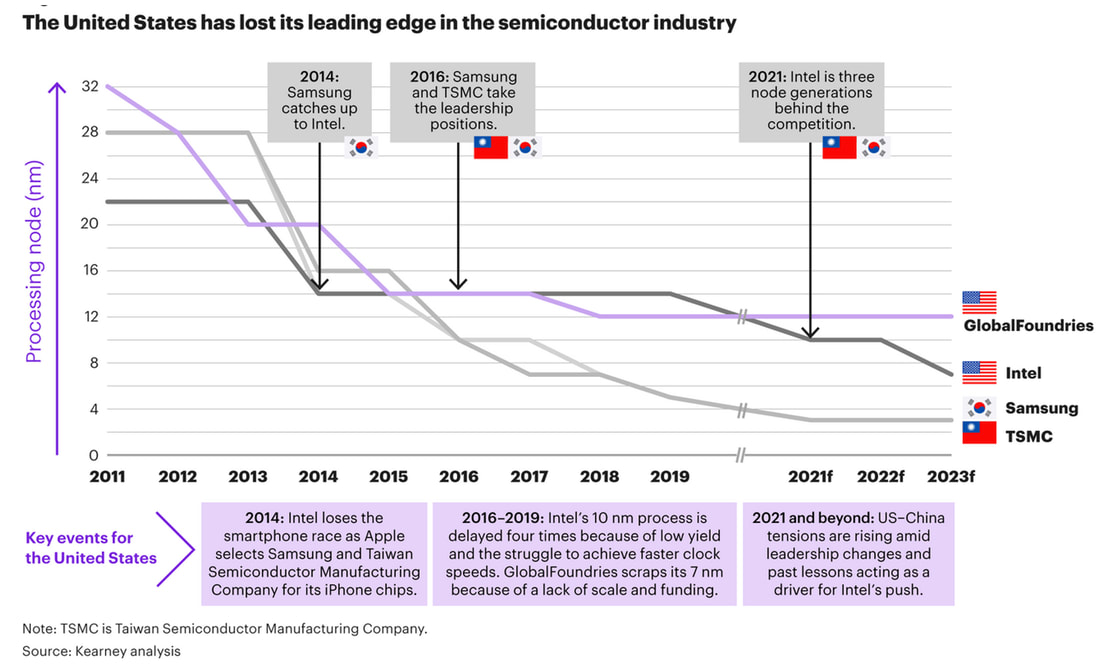

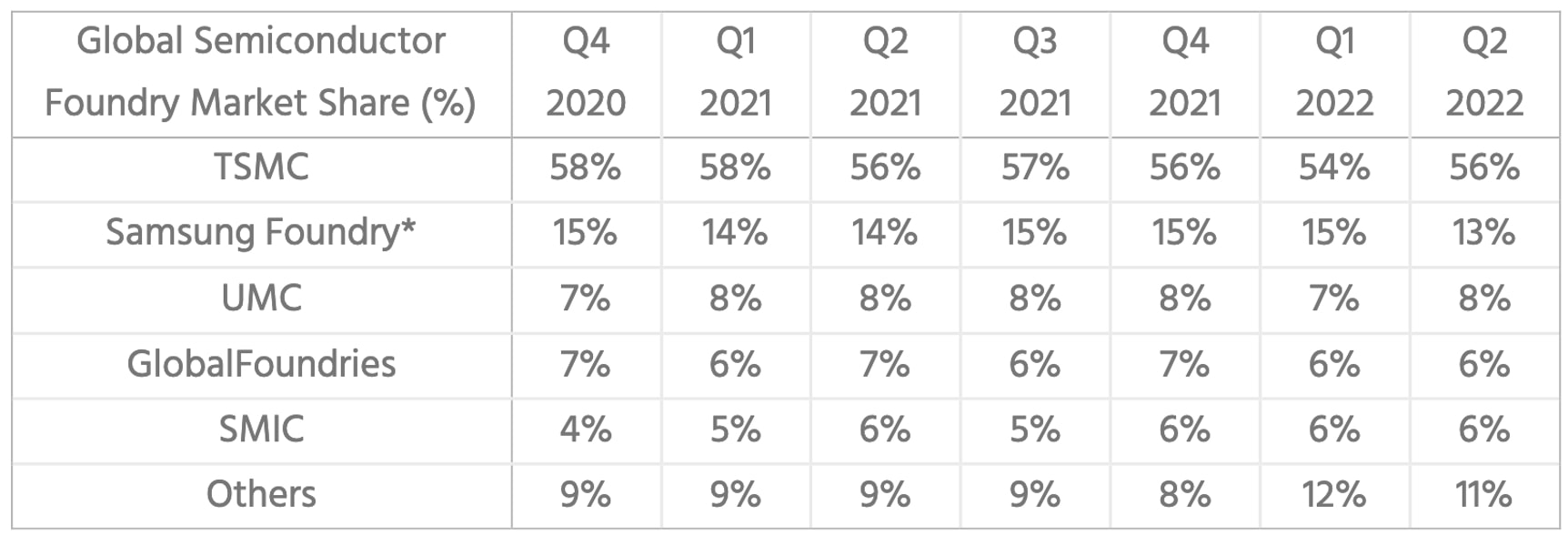

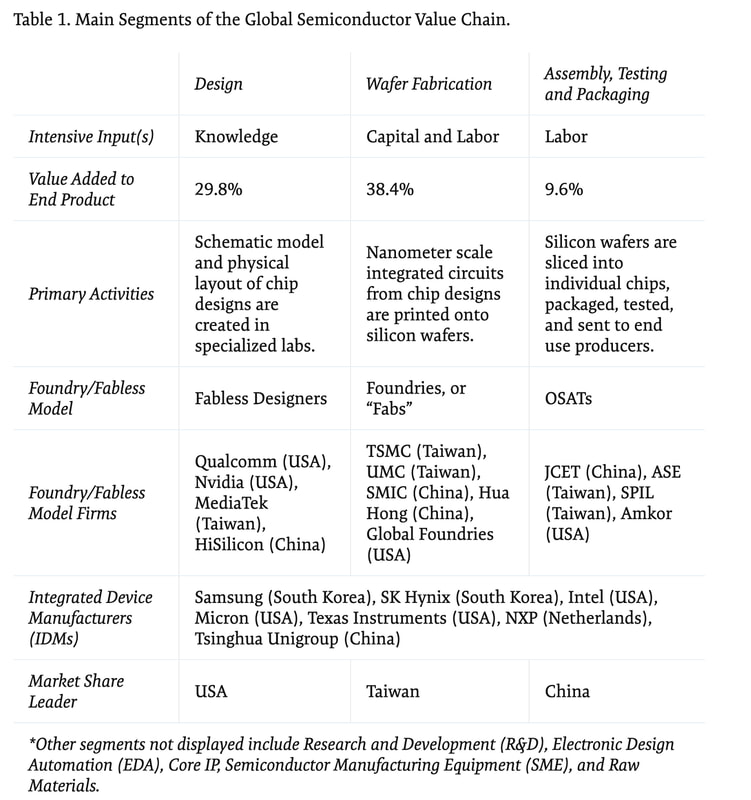

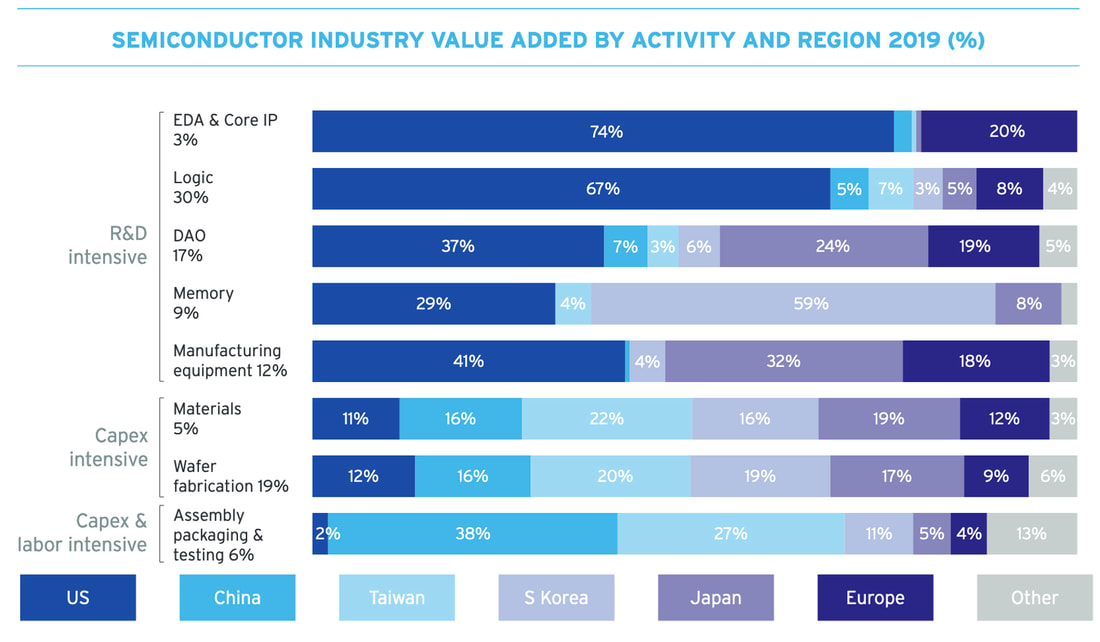

Zero production of advanced chips in America At a ground breaking ceremony for Intel’s new mega plant for leading edge chips fabrication in New Albany, Ohio, President Biden talked of the need to restart microchips production in the U.S. “… over 30 years ago, America had more than 30 percent of the global chip production. Then something happened. America ba- — America production, the backbone — the backbone of our economy — got hollowed out. Companies moved jobs overseas, especially from the industrial Midwest. And as a result, today we’re down to producing barely 10 percent of the world’s chips, despite leading in chip research and design.” The situation is even worse in relation to the production of the most advanced leading-edge microchips. President Biden: “Unfortunately, we produce zero — zero — of these advanced chips in America. Zero. And China is trying to move way ahead of us in producing them.” The U.S. versus the Rest A Kearney report from 2021 show the sorry state of microchips or semiconductor production in the U.S.  According to CSIS (Center for Strategic and International Studies) 75 percent of the world’s chips production is concentrated in North East Asia. Taiwan is in fact the centre of fabs (factories or foundries for fabricating chips) for advanced chips production, with the leading company TSMC earning a 56 percent market share of chips production worldwide. A table from Counterpoint show the market shares of the main foundries:  UMC’s (United microelectronics Corporation) is also located in Taiwan, while GlobalFoundries could be said to represent the West with fabs in US, Singapore and Europe. Chinese SMIC is a state-owned Chinese company. While advanced chips production in so-called called fabs or foundries is indeed in a sorry state in the U.S., at least for now, the situation is very different with regard to a different segment of the semiconductor value chain related to: Knowledge intensive semiconductor R&D, EDA (Electronic Design Automation, DAO (Discrete, Analog, and Other), Memory, SME (Semiconductor Manufacturing Equipment). In these areas the US is still leading with no close competitor. A CSIS table demonstrate geographical split in the main segments of the chips value chain (making up about 78 percent of whole value chain):  A bar chart from SIA (The Semiconductor Industry Association) show a more detailed picture for the three main segments: Knowledge intensive R&D, Capital intensive production, and Capital-intensive and Labour-intensive production.  While it is evident that the U.S. and to lesser degree Europe is leading in the knowledge intensive R&D segment, it is also clear that that fabs for fabricating semiconductor chips is concentrated in North East Asia, with Taiwan in the dominating position. The more labour-intensive assembly into finished products is shared between China and Taiwan. Especially notable is Taiwan’s leading position in the fabrication of the most advanced leading edge semiconductor chips. In the fabrication the of sub 10 nm (nanometre) semiconductor chips Taiwan has a share of 92 percent while South Korea is sitting on the rest. Just an example, the new iPhone 14 pro is built with chips using a 4 nm process made in Taiwan. Biden was certainly right when stating that there is no fabrication of leading-edge semiconductors in the U.S. at the moment. “There is currently no cutting-edge logic capacity below 10 nanometre being done in the United States.” (SIA). Why did this happen? How come that the U.S. and the rest of the World has become so dependent on advanced semiconductor chips fabricated in Taiwanese fabs and assembled into finished products in China? In a way the explanation is quite simple, labour costs are lower compared to the U.S. and Asia has a skilled workforce. That is why labour-intensive semiconductor production over the years became located in Taiwan, South Korea and China. Like so much else in manufacturing. It is not only labour cost that explains the movement to North East Asia. It is also government support and the characteristics of the labour force. “With decades of industrial policy support, robust infrastructures, and highly skilled workforces, Taiwan and South Korea are particularly strong in advanced manufacturing and possess a combined 100 percent of the global fabrication capacity in 7- and 5- nanometres processing nodes.” Chips for America That the present global regional division in the different segments is posing a growing problem for the U.S. and the West in general has become evident due to the simmering U.S. trade war with China. The situation is exacerbated by U.S.-China tensions related to Taiwan. No wonder the U.S. is eager to bolster U.S. competitiveness in relation to China. With Taiwan in a precarious position in relation to China, and with the dependence on both Taiwan and China for capital- and labour-intensive production and assembly of advanced semiconductor chips the U.S. and the West in general has a growing problem. Just think of the consequences of a possible Chinese blockade of Taiwan by air and sea. Or even worse China’s annexation of Taiwan. Cutting off the rest of a World and causing turmoil in the West with its insatiable appetite for chips from Taiwanese fabrication and Chinese assembly. “If China were to invade Taiwan, the most-advanced chip factory in the world would be rendered “not operable,” TSMC’s executive chairman Mark Liu has warned. No wonder then that the U.S. is very eager to re-nationalise the most import parts of those segments of the semiconductor chips production that is concentrated in Taiwan and China, or at the very least moving production to other countries, like Vietnam and India. We see the consequences of the outsourcing of production and supply of something that is absolutely vital for Western economies and their security. It has created a dependence on what is more or less a single source located far from home in a region where the potential for conflicts is growing steadily. No wonder that the U.S. and the West in general suddenly realised the precarious situation they are in with present shortage of semiconductor chips. In addition to a growing realisation that the extreme dependence on an Asian source of semiconductor chips might endanger Western economies and Western security. The energy shortage in Europe today shows the consequences of becoming on a single source of supply. Relaying on cheap natural gas the supply from Russia has suddenly become a major problem for Europe due its active engagement in a proxy war against Russia. The need for Action A letter to congressional leaders sent on December 1, 2021, by a broad coalition of 59 U.S. CEOs and senior executives, calls for action to ensure the supply of semiconductors vital to virtually all sectors of the economy – including aerospace, automobiles, communications, clean energy, information technology, and medical devices. They refer to the present global chip shortage resulting in lost growth and jobs in the economy. “The shortage has exposed vulnerabilities in the semiconductor supply chain and highlighted the need for increased domestic manufacturing capacity.” To alleviate the shortage, they urge “Congress to take prompt action to fund the “Creating Helpful Incentives for the Production of Semiconductors” (CHIPS) for America Act and enact a strengthened version of the “Facilitating American Built Semiconductors” (FABS) Act to include an investment tax credit for both design and manufacturing.” (semiconductors.org). And Congress listened and acted. The CHIPS and Science Act of 2022 In an effort to alleviate the chips shortage and re-establish the production of advanced microchips in the U.S. Congress recently introduced “The CHIPS and Science Act.” Also known as “Chips Act of 2022” it was signed on by Biden on August 9, 2022. It will allocate $52.7 billion for a “CHIPS for America Fund.” This includes: $39 billion to be used for manufacturing incentives, including $2 billion to focus solely on legacy chip production to advance economic and national security interests. For instance legacy chips used in cars and defense systems. $ 13.2 billion to be used for R&D and workforce development, including for Department of Defense-unique applications—and for semiconductor workforce training. $500 million for a “CHIPS for America International Technology Security and Innovation Fund” … for the purposes of coordinating with foreign government partners to support international information and communications technology security and semiconductor supply chain activities. . In a speech Biden emphasised that the “CHIPS and Science Act” was not just handling out blanks checks to companies: “I’ve directed my administration to be laser-focused on the guardrails that will protect taxpayers’ dollars. And we’ll make sure that companies partner with unions, community colleges, technical schools to offer training and apprenticeships and to work with small and minority- owned businesses as well.” Guardrails are also meant to ensure that recipients do not use the funds to build facilities in China and other countries of concern, and to prevent companies from using the funds for stock buybacks or shareholder dividends. To get support from the fund the recipients must also demonstrate significant worker- and community investment, in order to ensure that semiconductor incentives support equitable economic growth and development. Amongst others the act requires companies building new chip facilities to offer the prevailing wage. “The funds will also support good-paying, union construction jobs by requiring Davis-Bacon prevailing wage rates for facilities built with CHIPS funding.” (Fact sheet, CHIPS Act). SIA (The Semiconductor Industry Association) of course applauded the “CHIPS Act”: “The bill’s investments in chip production and innovation will strengthen America’s economy and national security – both of which rely heavily on chips – and reinforce our country’s semiconductor supply chains … The CHIPS Act will help usher in a better, brighter American future built on semiconductors.” https://www.semiconductors.org/sia-applauds-house-passage-of-chips-act-urges-president-to-sign-bill-into-law/ A European CHIPS Act On February 8, 2022, The European Commission proposed a “European Chips Act” to confront semiconductor shortages and strengthen Europe’s technological leadership.mEurope being in a worse bind than the U.S. with regard to chips shortage and lack of a European production of advanced semiconductor chips. (See the previous SIA bar chart). What does the Commission propose: “With the European Chips Act, the EU will address semiconductor shortages and strengthen Europe’s technological leadership. It will mobilise more than €43 bn of public and private investments and set measures to prepare, anticipate and swiftly respond to any future supply chain disruptions, together with Member States and our international partners.” What the Commission aims to do sounds like little more than a wish list at the moment, as can be seen from these vague aims.  https://ec.europa.eu/info/strategy/priorities-2019-2024/europe-fit-digital-age/european-chips-act_en The race is on. Other countries are planning to invest more in semiconductor manufacturing. Japan has approved a 774 bn yen (around 5.4 bn dollars), for semiconductor investments, and South Korea likewise is planning large semiconductor investments. Signs of change The early signs of government support for building new fabs for manufacturing semiconductor chips in U.S. has already led to a small wave of big announcements for new fabs. Here just a selection: As early as May 2020 TSMC (The Taiwan Semiconductor Manufacturing Company) announced it was going to build a $12.2 bn chip fab in Arizona. The first of its kind to mass produce 5nm chips in the U.S. In July 2022 TSMC placed the last beam in their Fab21 building in Phoenix Arizona. Expecting mass production of leading edge chips to begin in 2024. In November 2021 Samsung announced its commitment to build a $17 bn fab in Texas, also to begin production in 2024. With the promise of receiving funding from the “CHIPS Act” Intel in January 2022 announced plan for a $20 bn fab in Columbus Ohio. In may 2022 Texas Instruments “broke ground” for a 30 bn 300mm wafer fab in Texas (A semiconductor wafer is a thin slice of semiconductor substance, like crystalline silicon, used for the making of integrated circuits.). Meanwhile Samsung in 2022 apparently announced plans for investing up to 192 bn over the next decades in 11 fabs in Texas. While these plans for fabs may lead to rejuvenation of advanced semiconductor fabrication in the US, spurred along by the CHIPS Act’s $52 bn and the realisation that further investments in North East Asia may carry a growing risk, all is not well for the U.S. The U.S. may not yet possess a sufficiently skilled workforce for the fabrication of advanced semiconductors, because the focus hitherto has been on creating expertise in chip design. The amounts to be invested in fabs and the creation of a skilled workforce may turn out to be insufficient in relation to the investments in Taiwan, South Korea and most of all China. And what if China came in possession of Taiwan’s fabulous fabs. CHIP 4 Realising perhaps that even for the US it will next to impossible to achieve chips self-sufficiency, the US has proposed a semiconductor alliance to include the U.S. and the three Non-Chinese Asian partners including Taiwan, South Korea and Japan. Such an alliance would, as we can see from previous discussion, include all segments of semiconductor production from design, fabrication of chips, to assembly and packing. Of course, it could also be seen as a way to limit and contain Chinese influence. For the time being a rather diffuse attempt, with built in contradictions. “The Diplomat” reports that South Korea might be wary of such an alliance due to the its relations with China. With China accounting for 60 Percent of South Korea’s semiconductor export, and South Korean chip giants Samsung Electronics and SK Hynix having invested billions of dollars in key manufacturing facilities in China. South Korea must of course fear Chinese retaliation if South Korea became active member of Chip 4. It must be assumed that Taiwan would be just as wary, looking to its own already strained relations with mainland China. Even Japan would have look to its own relations with China, its exports and investment, and may not won’t to get too close to an alliance with Taiwan for these reasons. While Chip 4 may represent a further step in the Biden administration’s efforts to contain China in the global competition for hegemony, it will have wary and reluctant partners, and may escalate the war on chips. Leading to unknown retaliation from China and thus further escalation. A spanner in the works for China The U.S. is not only investing in leading edge chips production at home, it is also trying to trying to throw a spanner into Chinese plans for winning the future semiconductor race, by attempts to make sure that China cannot have access to leading edge semiconductor design and technology. A start had already been made by the Trump administration. In May 2019 it issued an executive order banning the Huawei Technologies Co. from buying vital U.S. technology without special approval and effectively barring its equipment from U.S. telecom networks on national security grounds. Later even Huawei’s non-America suppliers of products had to stop the exporting to Huawei if their products contained U.S. technology. The ban has been upheld by the Biden administration and has been a big blow to Huawei and its technologies, its products and of course its share price. In effect hampering Huawei’s technological development and worldwide sales. Today U.S. is going much further in its efforts to hamper Chinese semiconductor fabrication and development. Since 2019 the U.S. has put pressure on The Netherland’s government in order make sure that the ASML company (Advanced Semiconductor Materials Lithography?) cannot export its more advanced systems to China. In July 2022, it was reported that Washington has pressured the Netherlands government to take the campaign against China to a new level, with attempts to further limit ASML’s engagement in China. What is means? ASML has near monopoly on the design and manufacture of the EUV (extreme ultra violet) lithography machines that are used to print the ultrasmall, complex designs on microchip wafers, part of the process to produce leading edge sub 10 nanometre chips. (Todays striving is for 3 and 2 nm). “ASML has sold a total of about 140 EUV systems in the past decade, each one now costing up to $200 million, ... The price tag for its next machine, called High NA will be more than $300 million.” Of course, the U.S. wants to make sure that China’s chip fabs cannot get access to this technology, instead having to do with less advanced UV machines that make it impossible to produce leading edge sub 10 mm chips. “Any additional restrictions would deal a bigger blow to China’s efforts to become more self-sufficient in chips. An embargo could also cripple its ambitions to make chips that are close to today’s state-of-the-art.” (electronicdesign.com). On August 12 the U.S. established new export controls on technologies that enable semiconductors, engines and power systems “to operate faster, more efficiently, longer, and in more severe conditions in both the commercial and military context” (BIS, Bureau of Industry and Security) “The four technologies covered by today’s rule include two substrates of ultra-wide bandgap semiconductors: Gallium Oxide (Ga2O3), and diamond; Electronic Computer-Aided Design (ECAD) software specially designed for the development of integrated circuits with Gate-All- Around Field-Effect Transistor (GAAFET) structure; and Pressure Gain Combustion (PGC) technology (BIS). Cryptic to most of us, but BIS has provided some explanation. Gallium Oxide allow semiconductors to work under severe conditions, important for miliary and space use. ECAD is used in designing, analysing, optimizing, and validating the performance of integrated circuits or printed circuit boards. GAAFET is the key to enable 3 nm and below technologies, allowing for faster and more energy efficient semiconductors. While PGC represents “a novel approach for significantly increasing the efficiency of aerospace propulsion systems and ground-based power systems.” (Paxton). These restrictions “will potentially have the greatest impact on the trade between China and the US compared to all other actions taken to date,” (IBS consulting). Not enough for the U.S. in their war on chips with China. Now they are trying to hinder Chinese development in the areas of artificial intelligence (AI). An area in which China is trying to push ahead of the U.S. On August 26 Nvidia, a multinational company making chips used for deep learning and AI, announced: “the U.S. government, or USG, informed NVIDIA Corporation, or the Company, that the USG has imposed a new license requirement, effective immediately, for any future export to China (including Hong Kong) and Russia of the Company’s A100 and forthcoming H100 integrated circuits. Later the Company has been allowed to continue development of one of its less advanced AI chips in China. Another company, AMD, has likewise had its export of MI250 artificial intelligence chips to China restricted. It certainly looks as if the U.S. is doing all it can to hamper Chinese semiconductor development and their use, not the least in AI applications. Really throwing a spanner in the China’s chips and AI development. Perhaps hoping to delay China ambitious plans to overtake the U.S. in AI. Alas, the U.S. war on China’s ambitious plans may have a negative impact on the U.S. itself. A recent study has found that a full decoupling or even a modest decoupling from China may have serious implications for the U.S. semiconductor industry and its workforce, as can be seen from this table (Understanding U.S.-China Decoupling, U.S. Chamber of Commerce 2021)  China’s riposte in the war on chips While China really cannot do much to avoid the U.S. attempts to hamper China’s semiconductor ambitions. It has reacted with angry words, and lobbying attempts in the U.S. Somewhat amazingly, given China’s own actions, the Chinese Ministry of Commerce is arguing that the CHIPS Act “comes with discriminatory clauses and seriously violates market laws and international economic and trade rules” (Global Times). The Chinese equivalent to SIA, the Chinese Semiconductor Industry Association, complained that “these provisions clearly deviate from the shared principle of being fair, open and non-discriminatory that the global semiconductor industry forged through practice over the past decades.” (Global Times). Wordy protests not really achieving anything. The real question is. What can and will China do fulfil its own ambitious plan to leapfrog the U.S? In the immediate future probably not much. Looking a bit further there seems to be two possibilities. A dangerous one and long term one. The dangerous one: China blockading or invading Taiwan might force the U.S. and the West into a quid pro quo with China. Opening export to China in return for access to Taiwanese fabs. Or it might result in a tit for tat escalation and war. Less dangerous in the short term is the Chinese goal to become the leader in selected aspects of AI in 2025 and the World leader in AI by 2030. China may outspend the U.S. in R&D, in STEM education (Science, Technology, Engineering, and Mathematics), in creating an enormous and highly skilled workforce, and in investing in leapfrogging startup companies. According the “Made in China Plan” China aims to achieve 70 percent self-sufficiency by 2025. To achieve that goal a national fund for investment in integrated circuits (The Big Fund) and 15 local government funds for IC development has been established with a combined amount of $73 bn according to a report from SIA: “This does not account for government grants, equity investments, and low-interest loans which exceeds $50 billion alone” (Taking stock of China semiconductor industry, SIA). According to the SIA Report China is also rapidly closing the gap in AI chip design, “due partly to fast growing demand from China’s hyperscale cloud and consumer smart device market and lower barriers to entry in chip design. Chinese fabless firms are now taping out 7/5nm chip designs for everything from AI to 5G communications.” China certainly has the ambition, and we are seeing their advances in the number of patents, for instance in relation 5G communication and quantum computing. On September 8, 2022 Asia Times reported that China’s government says it will use the advantages of its “new-type whole-nation system” to catapult technological progress. Apparently meaning in translation: “That in order to improve the new nationwide system for tackling key and core technologies, it is necessary to organically combine the government, the market, and society, to scientifically plan, concentrate, optimize the mechanism, and coordinate tackling problems.” (From meeting of the Chinese Communist Party September 6, 2022). Whatever that means. The warning from history The South Korean giant Samsung’s remarkable example of leapfrogging the Japanese in the technological development and production of Memory chips (DRAMs), demonstrates that leapfrogging is possible. But it is certainly a very specific example of leapfrogging under rather favourable circumstances, where there is no serious attempt to contain the Korean leapfrogging. Perhaps a historical example of leapfrogging under more difficult circumstances may show that it is impossible to contain and restrict new technologies to a single geographical region by export restrictions and other means when there is growing demands for these products. (like in China today). Take the historical example of America colonies (later the U.S.) overtaking Britain in industrial textile manufacturing as an example. The rapid industrialisation of Britain the eighteenth and nineteenth century was fuelled by British advances in textile manufacturing, steam power and iron-making.Up to mid nineteenth century it was also a period where ideas of mercantilism were prevalent. A system of political economy that sought to enrich the country by restraining imports and encouraging exports of finished goods. Taking the example of the all-important textile industry it meant that Britain wanted to export all it could of the finished products, while trying its best to make sure that production knowledge, machines and artisans used to manufacture the products stayed in Britain. “Once British entrepreneurs had demonstrated the superiority of machinery in the manufacture of textiles, in the decades following the inventions of Hargreaves, Arkwright, Crompton and Cartwright, traditional efforts to contain British technology withing the kingdom was intensified. Checks against the outflow of Britain’s early industry were applied both by private businessmen and the government.” (Damming the Flood. David I. Jeremy). For a time, it became illegal to export industrial textile, metalworking, clock making, paper making and glass manufacturing equipment. Not only the export of machinery for textile production was banned. No skilled artisans and manufacturers in the textile industry were legally free to leave Britain or Ireland to carry out their trade in other countries. “Textile printing workers were even forbidden to leave the British Isles.” While some of these restrictions may remind one of the U.S. efforts to prevent the export of advanced semiconductors to China, at least similar restrictions do not (yet?) apply to people in the industry. Did Britain succeed in its attempts to make sure that the American colonies, from where the raw cotton for the textile production came, could not establish their own textile industry? No of course it didn’t. “During the revolution, American envoys in Europe accelerated efforts to steal technology and attract artisans. These initiatives continued during the Confederation period when both voluntary and official bodies attempted to speed technology transfer. The Pennsylvania Society for the Encouragement of Manufactures and the Useful Arts, for example, underwrote the establishment of a textile factory near Philadelphia and its leading official Tench Coxe helped smuggle over the technology. Coxe urged the Continental Congress to provide long-term monopolies to persons who introduced foreign technology, and he favored land grants as a lure to potential immigrants.” (Doron Ben Natar). And the lures seemed to work. In 1789 one Samuel Slater, working as a supervisor at one of the advanced English water-powered cotton mills, embarked on a ship bound for America, lured by the bounties offered for workers who knew how to manufacture cotton textile. Slater carried no written plans for cotton mills with him, as he risked being searched when leaving Britain, but he had apparently memorized everything he knew about Arkwright’s inventions in water-powered cotton mills and the first industrial examples of the division of labour to make cotton textiles. Slater built the first American cotton mill, paving the way for an American cotton textile industry. There were others like him and with that Ben Natar concludes “the United States emerged as the world's industrial leader by illicitly appropriating mechanical and scientific innovations from Europe" Sound familiar doesn’t it. Remember the Trump administrations accusation that China was illegally appropriating knowledge and technologies from the U.S. “The theft of intellectual property by international actors represents a massive threat to the American economy. In 2017, the Commission on the Theft of Intellectual Property estimated that intellectual property theft inflicted a cost of somewhere between $225 billion and $600 billion annually on the American economy, with China the primary culprit. The scale of some individual instances of theft can be downright staggering—in one notable case, a Chinese company stole as much as $8.75 billion in microchip technology from Idaho-based Micron.” Britain could neither keep Industrial knowledge, machinery or people at home, and it even became an important investor in the industrialisation in America, not the last in the rapid growth of railroads. And soon investments and inventions in the U.S. leapfrogged British industry. “A golden torrent of British capital flowed abroad from 1870 to 1914, annually averaging about a third of the nation’s investment. In 1913, 32 percent of Britain’s wealth (a total of £4 billion at the time) was vested in overseas assets, primarily the bonds of railroads and utilities in the United States, Argentina, and other settler regions.” (The decline and fall of the British economy, D. Kedrosky). Somewhere around the 1870’s the U.S. overtook Britain in manufacturing. To compare with the present. Something similar seems to be happening in relation to China and the U.S. today. Similar to the flow of investments from Britain to the U.S. manufacturing in China is accompanied by an influx of foreign investments. According to the “Peterson Institute for International Economics” foreign direct investment in China grew to $334 in 2021, an all-time high. In recent years China has thus become the manufacturing hub of the World. China accounts for around 29 percent of global manufacturing output, while the U.S. has slipped to 17 per cent and followed by Japan and Germany.(Statista).  “China ranks first in terms of share of global output in 16 categories of 22 manufacturing categories tracked by the U.N., while second in six others. The data is from 2019, the most recent year available. China continues to dominate in light industries such as apparel and textiles, general sectors like basic metals and electrical equipment, and higher-end activities like computers and transport equipment. There’s hardly a sector in which China does not have at least a 20% global market share, while commanding 40%+ shares in electrical equipment, basic metals and computers. In textiles, apparel and leather, China’s share is more than half.”(Barrons). As we seen China is not yet a champion in the production of advanced semiconductors, but then we have to remember that Taiwan is, and China insists that there is only one China and Taiwan is part of it. And if that also became the reality, China would jump to the front in the production of advanced semiconductors. Production that is, not yet design. But China might be on the verge of overtaking the U.S. in areas related to Artificial Intelligence or AI. A final report on AI from the U.S. National Security Commission on Artificial Intelligence (NSCAI) published in 2021 concludes: “The leading indexes that measure progress in AI development generally place the United States ahead of China. However, the gap is closing quickly. China stands a reasonable chance of overtaking the United States as the leading center of AI innovation in the coming decade. In recent years, technology firms in China have produced pathfinding advances in natural language processing, facial recognition technology, and other AI-enabled domains.” Does history repeat itself? Not one to one of course. We are no longer talking textile machinery, but advanced semiconductors and AI. Looking at the data we have shown that it certainly seems probable that in the war on chips China might overtake the U.S. and thus the West. The present U.S. sanctions restrictions may hamper Chinese development in these areas, but also encourage Chinese to search for ways to leapfrog the U.S. based on their own efforts. Like the British attempts to prevent the growth of textile manufacturing in the colonial US and later in India, it may prove impossible to stop the colossal Chinese momentum, in research, investment and production. The U.S. realization that China might soon overtake the U.S. in AI may represent the writing on the great wall. A kind of mene mene tekel upharsin for the West. Comments are closed.

|